About 2 month ago, I accidentally stumbled on the Dave Ramsey Show on Youtube. I got hooked on it and ended up watching over an hour of his show. I immediately got the book (The Total Money Makeover: A Proven Plan for Financial Fitness ). I finished reading the book within a week and I felt that how I would have turned out if I got this book in earlier age. I am not sure if I would have been financially free but I think I would have became much better than where I am now. However, nothing is never late!

). I finished reading the book within a week and I felt that how I would have turned out if I got this book in earlier age. I am not sure if I would have been financially free but I think I would have became much better than where I am now. However, nothing is never late!

But… after 2 month, I started to get different thoughts. Here is why.

The book tells many insights of how an ordinary person with an annual average income ($40k to $60k) person can be financially free. It was brilliant. It opened my eyes in different view.

Following is my summary of the book.

- 7 baby steps to be financially free.

- Baby Step 1 – $1,000 to start an Emergency Fund

- Baby Step 2 – Pay off all debt using the Debt Snowball

- Baby Step 3 – 3 to 6 months of expenses in savings

- Baby Step 4 – Invest 15% of household income into Roth IRAs and pre-tax retirement

- Baby Step 5 – College funding for children

- Baby Step 6 – Pay off home early

- Baby Step 7 – Build wealth and give!

- How to approach the 7 baby steps.

- Don’t spend money now so that you can spend later.

That’s it. There are tons of success stories and they are very inspiring. The main idea of the book is to be financially free with what you currently have. If you have a car or house that is more than what you can afford, then you get rid of the it and buy an used car that you can pay with cash or move somewhere you can afford. Then, you become a very frugal person to pay off all debt.

At the time of reading the book, I had my proud Porsche Cayman S. It was a gift to myself. I paid in cash. However, within a few weeks after reading the book, I sold the car in order to pay off my home. I had couple thousands of student loan. I paid that off first. I never carry any balance on my credit card. Well, I was debt free within a day except the mortgage. I bought my wife an used Scion xB and I got an used Honda Civic GX. I was already on 4th step of 7 steps in 1 day.

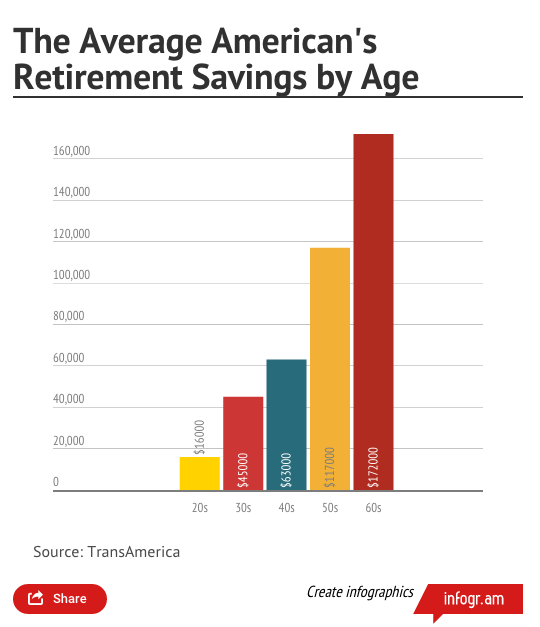

Step 4 is where I stopped. All the saving methods for retirement. Hum…

RothIRA. Good idea if you started very early. I personally think that any index based investment is not in good timing. Yes, DJIA now is above 20,000 and I am a firm believer that it’s bubble. Do I have money in stock? Yes I do. It’s because I can always pull it out without penalty (except capital gain tax). RothIRA? I am stuck for long time.

So, here is what I am considering for retirement.

I know that price of house has been increasing. As matter of fact, the average price of house is getting almost close to the price just before subprime mortgage time in 2008.

I personally think that this price is also bubble. I think it would increase for another year or two. Why? One of my neighbor put their house for sale. $450,000. I literally laughed at the price. Don’t get me wrong. It’s pretty decent neighbor and nice area to live but even for myself, I would not purchase this home for 450k. The house was out in the market for a month and not sold yet. That tells me that people are thinking that the price of house is getting close to the peak. Also, there is another house that I have been putting my eyes on. It was on market couple month ago for 750k, then it didn’t sell. The same house came out on market just today for 830k. Hum… The house is nice with 3 car garage, 4 bedrooms, huge backyard with RV pad with separate RV gate, and area of 9000 sq ft lot. Um… for 830k, I can buy any house just like that. I don’t think the house will be sold for that price.

So? My plan is to save up and buy next house in cash during next dip. I am planning to keep increase the rental properties until it replaces my income. That income will be my retirement fund. No IRA for me.

Final thoughts?

You must read The Total Money Makeover: A Proven Plan for Financial Fitness and see how it’s like. It would open eyes for sure. I also got hold of The Total Money Makeover Workbook . It gives step by step guide to follow 7 baby steps. It’s really good book to have if you want to see the different version of The Total Money Makeover: A Proven Plan for Financial Fitness. To my view, both books are exactly the same except the workbook laid out in such way that you can write and check each steps. Dave Ramsey also has class that you pay and attend. I found audio version on online and listened some. It’s exactly the same as The Total Money Makeover: A Proven Plan for Financial Fitness in live version. I wouldn’t spend 9 days over 9 weeks time when you can read the book in a day or two if you can really focus on the book.

. It gives step by step guide to follow 7 baby steps. It’s really good book to have if you want to see the different version of The Total Money Makeover: A Proven Plan for Financial Fitness. To my view, both books are exactly the same except the workbook laid out in such way that you can write and check each steps. Dave Ramsey also has class that you pay and attend. I found audio version on online and listened some. It’s exactly the same as The Total Money Makeover: A Proven Plan for Financial Fitness in live version. I wouldn’t spend 9 days over 9 weeks time when you can read the book in a day or two if you can really focus on the book.

Below is some bullet points from the book that I would keep refer to.

• Auto and Homeowner Insurance—Choose higher deductibles in order to save on premiums. With high liability limits, these are the best buys in the insurance world.

• Life Insurance—Purchase twenty-year level term insurance equal to about ten times your income. Term insurance is cheap and the only way to go; never use life insurance as a place to save money.

• Long-Term Disability—If you are thirty-two years old, you are twelve times more likely to become disabled than to die by age sixty-five. The best place to buy disability insurance is through work at a fraction of the cost. You can usually get coverage that equals from 50 to 70 percent of your income.

• Health Insurance—The number-one cause of bankruptcy today is medical bills; number two is credit cards. One way to control costs is to look for large deductibles to lower your premium. The HSA (Health Savings Account) is a great way to save on premiums. The high deductible creates a much lower premium, and this plan allows you to save for medical expenses in a tax-free savings account.

• Long-Term Care Insurance—If you are over sixty, buy Long-Term Care insurance to cover in-home care or nursing home care. The average nursing home stay costs $40,000 per year, which will crack and scramble a nest egg in a heartbeat. Dad in the nursing home can use up Mom’s $250,000 savings in just a few short years. Make your parents get it.

– I don’t recommend selling your home unless you have payments above 45 percent of your monthly take-home pay.

– if you can’t be debt-free on it (not counting the home) in eighteen to twenty months, sell it.

– Growth and Income funds get 25 percent of my investment. (They are sometimes called Large Cap or Blue Chip funds.) Growth funds get 25 percent of my investment. (They are sometimes called Mid Cap or Equity funds; an S&P Index fund would also qualify.) International funds get 25 percent of my investment. (They are sometimes called Foreign or Overseas funds.) Aggressive Growth funds get the last 25 percent of my investment. (They are sometimes called Small Cap or Emerging Market funds.)

– I suggest funding college, or at least the first step of college, with an Educational Savings Account (ESA), funded in a growth-stock mutual fund. The Educational Savings Account, nicknamed the Education IRA, grows tax-free when used for higher education. If you invest $2,000 a year from birth to age eighteen in prepaid tuition, that would purchase about $72,000 in tuition, but through an ESA in mutual funds averaging 12 percent, you would have $126,000 tax-free. The ESA currently allows you to invest $2,000 per year, per child, if your household income is under $220,000 per year. If you start investing early, your child can go to virtually any college if you save $166.67 per month ($2,000/year). For most of you, Baby Step Five is handled if you start an ESA fully funded and your child is under eight.

– When refinancing, ask for a “par” quote, which means zero points and zero origination fee.